The 2026 Material Pivot: Why Morgan Stanley is Bullish on Lithium & Uranium

Bearish on Solar

If you’ve been watching the commodities space, you know it’s been a volatile year. But a fresh research note from Morgan Stanley (dated Dec 15, 2025) on the Asia Pacific Materials sector just hit my desk, and it paints a very specific picture for the year ahead.

The broad narrative for 2026 is shifting. We are moving from a general “Green Energy Boom” to a market of extreme divergence.

The Big Takeaway

Morgan Stanley’s team, led by Rachel Zhang, has identified a clear split in the “New Materials” sector:

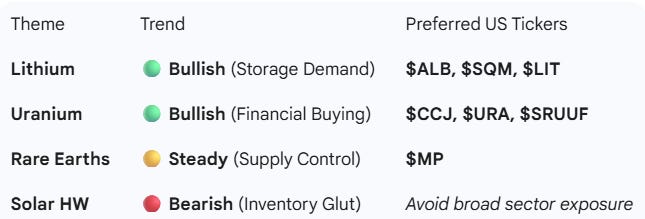

Lithium & Uranium: The bottom is in. Demand is surprising to the upside. (Bullish)

Solar Glass/Components: The hangover from the 2025 rush is real. Inventory is piling up. (Bearish/Cautious)

Let’s dig into the details.

1. The Return of Lithium (It’s Not About EVs, It’s About Storage)

For the last 18 months, the lithium narrative has been plagued by oversupply fears. That narrative is dead.

The Catalyst:

According to the report, Lithium demand has outperformed expectations YTD, driven not just by cars, but by Energy Storage Systems (ESS).

The Data: ESS production is up 70% YoY in 2025, with another 50% growth expected in 2026.

The Price: Lithium Carbonate prices in China have recovered to nearly RMB 100k/t.

Supply: Supply discipline is holding. Several mines (specifically lepidolite mines in Yichun) remain at risk of shutdown, keeping a floor under prices.

The US Trade

If the Chinese spot price is recovering due to massive storage demand, the arbitrage for Western miners is clear. The “balanced supply-demand” outlook for 2026 is a green light for the beaten-down majors.

Albemarle (ALB): As the global leader, ALB is the highest beta play to a recovery in spot prices.

Arcadium Lithium (ALTM): A pure-play miner that benefits immediately from the improved sentiment mentioned in the MS report.

ETF Play: Global X Lithium & Battery Tech ETF (LIT).

2. Uranium: The Momentum Trade

The report highlights “Strong Uranium Price Momentum” going into 2026. The thesis here is structural.

The Catalyst:

Financial Buying: Major investment vehicles (like SPUT and Yellow Cake) are expected to resume buying in the spot market after the holiday season.

The Squeeze: Long-term prices hit $86/lb at the end of November.

Upcoming Event: Keep an eye on January/February 2026. Kazatomprom (the world’s largest producer) will announce production guidance. Any disappointment there acts as a massive catalyst for price spikes.

The US Trade

The report explicitly likes CGN Mining (HK listed), but for US portfolios, the correlation is direct:

Cameco (CCJ): The Western heavyweight. If Kazatomprom has issues or prices rise, Cameco wins.

Sprott Physical Uranium Trust (SRUUF / U.U): The report mentions “SPUT” directly. This is the mechanism tightening the physical market.

Uranium Energy Corp (UEC): For those seeking higher leverage to spot price moves.

3. Rare Earths: The Geopolitical Hedge

Rare earth prices remain strong due to “tightened supply-side controls” in China. With export licenses normalizing but control remaining strict, prices are elevated.

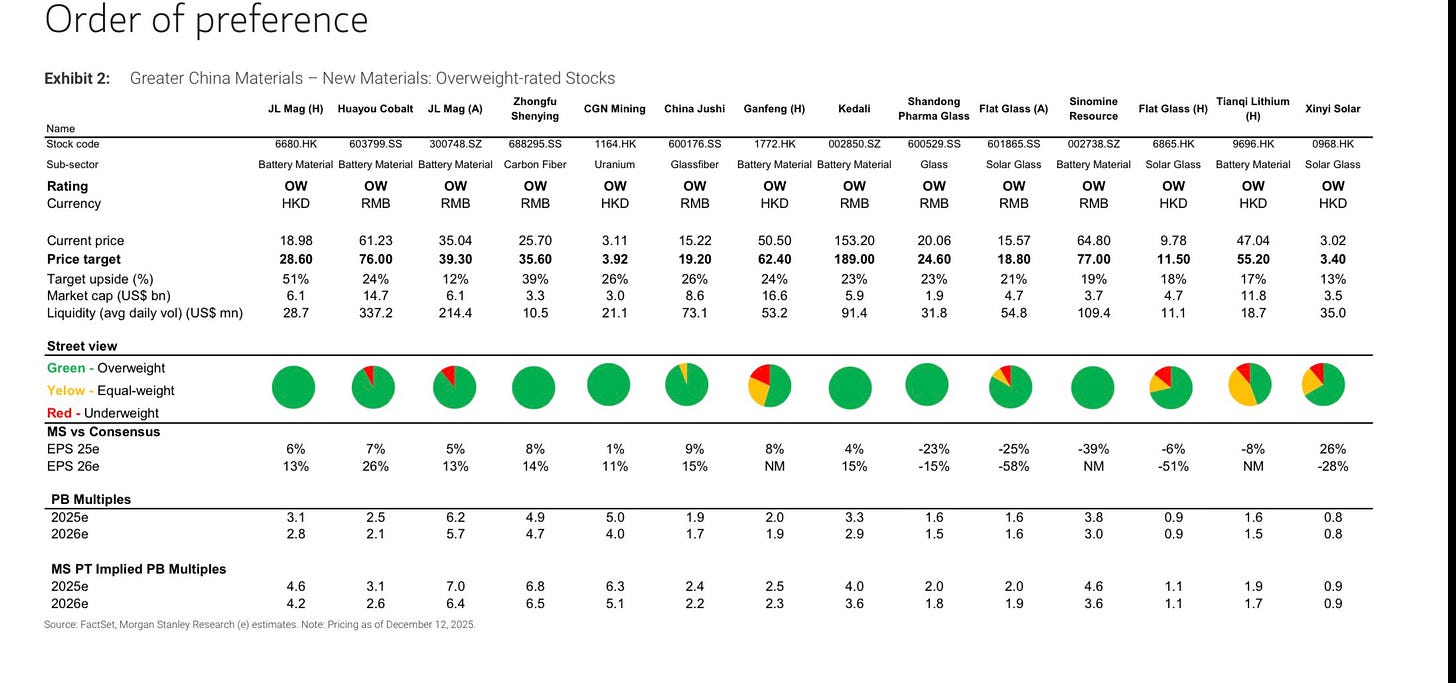

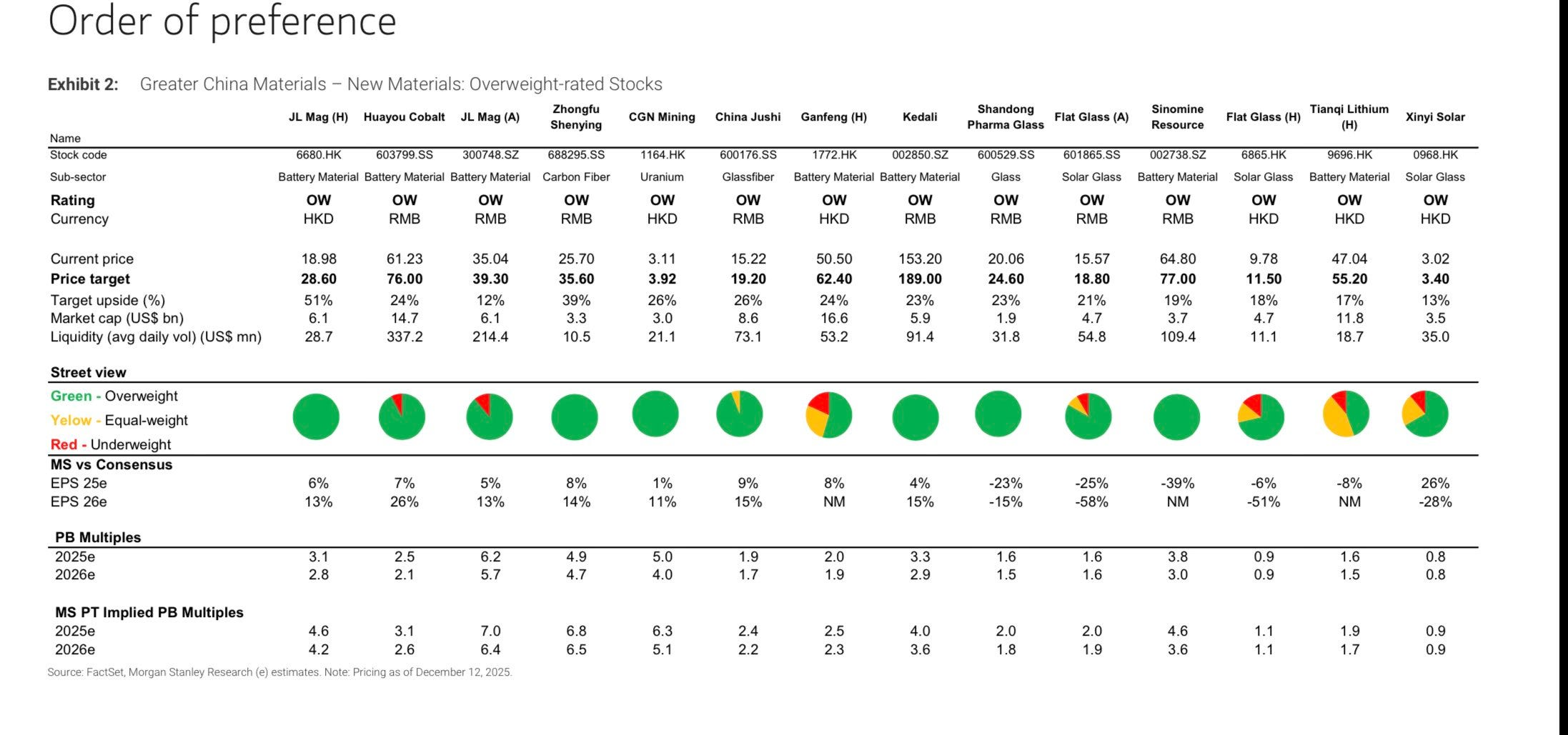

The Chart: JL Mag (6680.HK) is shown in Exhibit 2 with the highest upside potential (+51%) among the covered stocks.

🇺🇸 The US Trade

When China tightens rare earth exports or prices rise, the strategic value of non-Chinese supply skyrockets.

MP Materials (MP): As the owner of the Mountain Pass mine, MP is the primary hedge against Chinese supply constraints.

4. Solar Glass: The Warning Sign

Here is where the report turns bearish. MS warns that “Weak demand remains an overhang.”

The Problem:

Demand Pull-Forward: 2025 saw “rush installations” to beat tariff reforms. This borrowed demand from 2026.

Inventory Glut: Industry inventory has piled up to ~31 days.

Oversupply: Supply is still at ~88kt/d, which supports far more production than the market needs.

The Verdict: “Capacity exits need to continue.” Translation: Companies need to go bust or shut down factories before this sector gets better.

The US Implication

Be very careful with solar hardware stocks right now. While the US market has different tariff dynamics (hello, First Solar), the global glut in solar glass and components usually compresses margins for everyone.

Avoid/Neutral: Generic solar component manufacturers exposed to global pricing pressure.

Summary: The 2026 Playbook

Based on the Morgan Stanley data, here is how I am positioning for the start of 2026:

The “Energy Storage” story is quietly overtaking the “EV” story as the driver for lithium. Don’t miss the forest for the trees.

[Disclaimer]

The content provided on this website is solely my professional analysis and personal observation of companies, industry trends, and financial conditions as of a specific date. It is for readers’ reference only and does not constitute any solicitation, inducement, buying or selling, investment advice, or guarantee of profit or loss.